The first point to make is that when there are huge stockmarket losses, other unrelated assets become a source of funds to cover them. In that context, the decline in gold from all-time highs is minor so far. Let’s look at the underlying position.

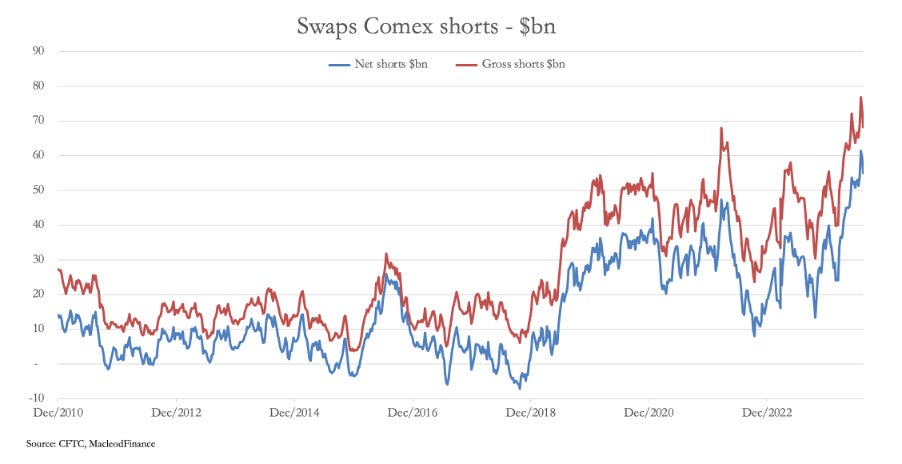

The big negative is the short positions on Comex and London. In the case of London, we must include unknown quantities of fractionally reserved unallocated accounts in European banks. But the visible position is obviously Comex, where the bullion bank trading desks are short. The position at the last Commitment of Traders numbers (30 July, when gold was $2410) is shown in the chart below:

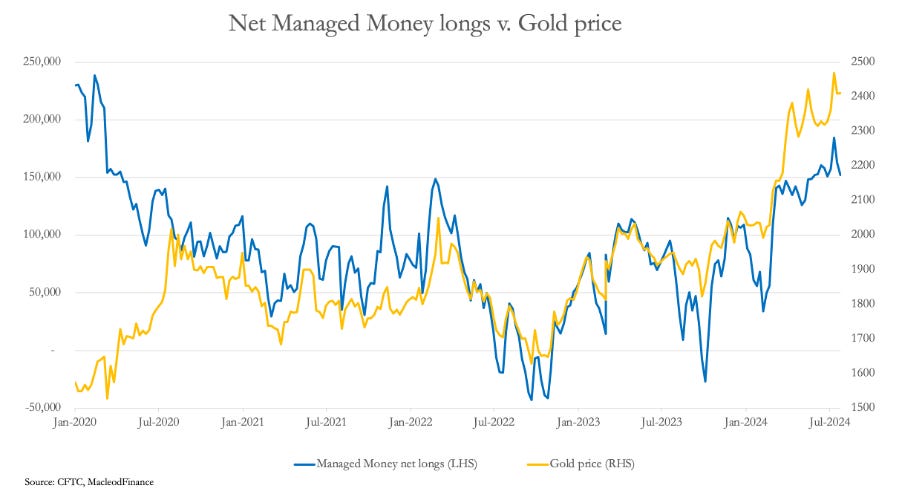

Swaps are mostly bullion bank traders, and there were 20 long, and 24 short. The short position was $68.2bn, averaging $2.84bn each, before any offset from the longs. These are close to a record, and some bank treasurers will be pushing to get these positions down. As a group, they have a common interest in aggressively taking out any and all speculator longs. They are net long 150,000 contracts, not overbought but marginally more than the long-term average which we take as neutral. They are shown next:

The current active contract is December, which allows the Swaps to push the price around because the December contract value doesn’t meet the spot price until end-November (which it does by being deliverable at that time).

How to Trade In Stocks

Best Price: $7.33

Buy New $13.53

(as of 10:43 UTC - Details)

How to Trade In Stocks

Best Price: $7.33

Buy New $13.53

(as of 10:43 UTC - Details)

A second negative is speculator longs on the Shanghai Futures Exchange, if these players are squeezed into losses on leveraged positions.

Against this, there are two very powerful positives. The first is that central banks, sovereign wealth funds, and Chinese banks offering gold accounts to their depositors are greedy buyers of physical bullion. We see evidence of this with Comex stands-for-delivery, with over 1,705,600 ounces (53 tonnes) stood for delivery in the last four trading sessions. At the same time exchange for physicals have swollen to 31,202 contracts in those sessions (equivalent of 3,120,200 ounces (97 tonnes). We can’t say that all EFPs are in the same direction, but it is likely to be mostly LBMA members exchanging Comex contracts for London forward long positions and delivery taken there. Undoubtedly, the big buyers using these facilities are Chinese banks operating on the PBOC’s and their own behalf.

A second positive is that ETFs held by the public in western capital markets have been sold down over the last few years. While there could easily be more selling from this quarter to cover losses in equity markets, it is unlikely to be a significant factor.

Silver

Rich Man Poor Bank: Wh...

Best Price: $7.43

Buy New $16.20

(as of 12:17 UTC - Details)

Not only is silver more volatile, but when gold is not actually rising and therefore reflecting an increasingly desirable haven for those fleeing weakening credit, the pause in “moneyness” allows the paper shorts to hit silver prices hard. This is why when gold has only declined 3%, silver has fallen five times as much, taking the gold/silver ratio to 88.3. Until gold begins to move ahead, one cannot rule out further weakness in silver. But when the shortage of physical starts driving gold prices higher, silver should soar like a rocket.

Rich Man Poor Bank: Wh...

Best Price: $7.43

Buy New $16.20

(as of 12:17 UTC - Details)

Not only is silver more volatile, but when gold is not actually rising and therefore reflecting an increasingly desirable haven for those fleeing weakening credit, the pause in “moneyness” allows the paper shorts to hit silver prices hard. This is why when gold has only declined 3%, silver has fallen five times as much, taking the gold/silver ratio to 88.3. Until gold begins to move ahead, one cannot rule out further weakness in silver. But when the shortage of physical starts driving gold prices higher, silver should soar like a rocket.

War

Tensions in the Middle East are rising astronomically, ignored by markets so far. Reports from credible analysts, and all westerners being told to get out of Lebanon, confirm that in the coming weeks there will be a serious escalation in the Israeli conflict involving not only Iran’s proxies, but Iran itself plus Lebanon and Syria. Russia and China are backing Iran and Syria, America and the UK backing Israel. By refusing any compromise with the Palestinians, Israel will be fighting for its very survival. If attacked, do not rule out Iran closing off the Hormuz Straits, which would drive the oil price through the roof.

Conclusion

Trade gold and silver at your peril. Stackers should just shut their eyes and continue stacking. It could be the last decent chance before gold hurdles well over $2,500.

Reprinted with permission from MacleodFinance Substack.