If you don’t think Washington is populated by the world’s greatest collection of idiots, just consider some of today’s incoming data, starting with another disastrous trade report.

The trade deficit in goods for August posted at -$89.4 billion, which is nearly the worst monthly figure on record and 40% below the already huge -$63.7 billion deficit posted for the pre-Covid peak in February 2020. And, no, we are not harping here on the trade account’s tsunami of red ink out of some Trumpian affection for protectionism.

To the contrary, this is the result of stupid economics – specifically the $6 trillion bacchanalia of Covid bailouts and stimmies enacted during the last 18 months. Self-evidently, the overwhelming share of that gratuitous add-on to spending flowed into the veins of international trade and came ricocheting back in the form of a $26 billion monthly increase in the goods deficit.

Xi Jinping is surely marveling at Washington’s endless capacity to keep his Ponzi alive every time it begins to unravel, as was the case in the spring of 2020.

Indeed, the blue line in the chart has been driven for the last 30 years by the massive deficit in goods with China. The latter, in turn, provided the hard currency earnings which enabled the Red Suzerains of Beijing to build a massive industrial economy from whole-cloth on the back of $50 trillion of debt.

In the ordinary course, of course, the Red Ponzi would have collapsed under the weight of egregious central bank money-printing and an unserviceable debt buildup years ago. But Washington is so smitten by the false economics of the printing-press dollar that it permitted its own rogue central bank to race the People’s Bank of China to the currency bottom, thereby enabling China’s flood of yuan to stay afloat on an even greater inundation of dollars.

US Trade Balance In Goods, 1992-2021

In the most recent Covid-interval, Washington simply added insult to injury, driving the blue line shown above ever deeper into the lower right hand zone of the chart. And it did so out of the misbegotten notion that whenever GDP falters – regardless of the reason – the course of first and only resort is to flood the zone with massive dollops of fiscal and monetary “stimulus”.

But for crying out loud. The approximate $1 trillion shortfall of nominal GDP from trend over the last six quarters is a result of a government ordered supply-side contraction. That is, the double-whammy of first lockdowns and then the endless propagation of Covid fears by the Virus Patrol that together set the social congregation sectors of the economy back on their heels for no valid reason.

That is to say, households curtailed their spending last year not because they ran out of cash and credit card capacity (i.e. demand), but because going to the bar, restaurant, movies, gym, hair salon, ball game etc. was illegal or perceived to be dangerous thanks to the endless fear-mongering of Dr. Fauci et. al.

Stupid and unnecessary as this state-ordered supply side contraction actually was – -still, so be it. If in its (un)wisdom Washington ordered a hiatus in normal GDP growth for the duration of the Covid, then that temporary gap in the great stream of history would have been little-noted nor long remembered.

Consumers who couldn’t go to restaurants three days a week were free to binge on home-cooking, Netflix, scrabble and backyard beanbag, as the case may be. The vast majority that remained employed and collected their paychecks were also free to replenish their savings and those which got laid-off could have been held harmless at 60-70% of normal pay by the regular unemployment system and a few hundred billion of Federal gap coverage.

The $6 trillion of Covid relief spending, therefore, amounted to staggering overkill that got channeled into goods–a high share of which are sourced abroad and imported.

The chart below is the smoking gun. The purple line shows that notwithstanding an economy that got knocked into a cocked-hat in 2020, household spending on durable goods has accelerated like never before, rising by 27% since February 2020. To put that in context, that’s a 17.3% annualized rate, and even when you squeeze out the 3.5% per annum gain in the CPI during the same period, the real gain is nearly 14% per annum.

In a word, real PCE on durable goods has never risen by 14% per annum over an 18 month period, even during the halcyon days of the 1960s. It happened only because Washington was mainlining consumers with massive dollops of stimmies and free stuff on top of what would have otherwise been their normal propensity to reallocate spending to durables from what would have otherwise gone to locked-down service sectors.

By contrast, PCE for services (brown line) experienced an unprecedented hiatus, rising by just 2.0% over the entire period. That is to say, nominal durables spending grew by 17.5% per annum, while services inched up by just 1.3% per annum, which after inflation actually amounted to a measurable shrinkage.

Alas, not a single dime of that services spending shortfall was owing to lack of household monetary wherewithal – they had plenty of idle cash and credit lines.

To the contrary, the red line in the chart shows merely the government ordered contraction of GDP in the social congregation sectors of the economy. There wasn’t anything wrong with “demand”, the animal spirits of consumers or the structure of the economy. So there was no need for demand stimulus, either.

At the end of the day, we surely have a case of small-minded politicos and government apparatchiks who have come to believe that any disturbance in the US economy amounts to a nail that needs be whacked good and hard with their stimulus hammer.

Personal Consumption Expenditures: Durables Versus Services, February 2020-August 2021

To be sure, the above madness is par for the course. All in a days work. And here’s another.

The price of cotton is soaring on the global market and is now up 60% from its April 2020 bottom, meaning more inflationary pressure is barreling down the supply pipeline. But in this case, Washington has actually made a farce out of stupidity.

In their arrogance, the passel of neocons and liberal interventionist who surrounded the Donald during his futile days in the White House, lowered the sanctions boom on China for the alleged human rights violations against the Uighur people in Xinjiang Province of western China, where much of the nation’s cotton is grown. Washington’s writ was that no apparel could be legally imported from China – where most of US apparel supply comes from – if it was made with Uighur-tainted cotton.

The result is that the Chinese apparel factories where forced to eschew their own domestic cotton and source on the international market mainly in the US – thereby driving up the price – so that they could continue to sell shirts, dresses, underwear and socks to America. Talk about a costly round trip of cotton bales that will do nothing for the Uighurs but will soon slam American consumers with another hefty dollop of inflation – this time in the cost of apparel.

International Price Of Cotton, February 2020-August 2021

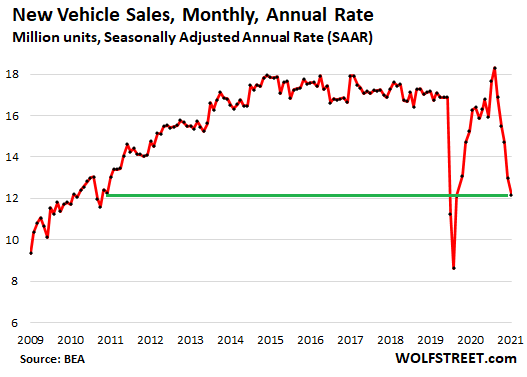

Finally, consider the collapse of auto sales depicted in the chart below. The August SAAR (seasonally adjusted annual rate) of 12.2 million was actually down by 29% from last year, and stood at nearly the Great Recession low of 2010.

Surely, consumers have the wherewithal and auto credit has never been cheaper and more abundant. The problem is, again, on the supply side. This time because a huge part of the auto parts supply chain has been off-shored during the past 30 years and the global supply chain is now roiled with imbalances and shortages.

Thanks, Fed.

Its ridiculous target of 2.00% domestic inflation is the culprit. Those auto parts, assembled cars and well-supplied dealer lots would actually still be operative on these shores if Washington had not crucified sound money on a cross of perpetual monetary stimulus.

PEAK TRUMP, IMPENDING CRISES, ESSENTIAL INFO & ACTION

Reprinted with permission from David Stockman’s Contra Corner.