Two recent surveys, along with numerous other studies and data, reveal most American households to be living on the brink of catastrophe, but continuing to act in a reckless and delusionary manner. There have certainly been economic factors beyond the control of average Americans that have resulted in real median household incomes remaining stagnant for the last 36 years. The unholy alliance of mega-corporations, Wall Street and bought off corrupt politicians have gutted the nation of millions of good paying jobs under the guise of globalization, while utilizing debt, derivatives and financial schemes to enrich themselves. The malfeasance of the sociopathic privileged class does not discharge the personal responsibility of citizens for living within their means. A lack of discipline, inability to delay gratification, failure to understand basic mathematical concepts, materialistic envy, absence of critical thinking skills, and a delusionary view of the world have left the majority of Americans broke and in debt.

The data that captured my attention was how little the average American household has in savings. Roughly 62% of Americans have less than $1,000 in savings and 21% don’t even have a savings account, according to a new survey of more than 5,000 adults conducted this month by Google Consumer Survey for personal finance website GOBankingRates.com. This dreadful data is reinforced by a similar survey of 1,000 adults carried out earlier this year by personal finance site Bankrate.com, which also found that 62% of Americans have no emergency savings for a medical crisis, car repair, or unanticipated household expenditure.

The fact is these are not highly unlikely scenarios. They happen every day as part of our routine existence. Everyone gets sick. Every car eventually needs new tires or an engine repair. Every home will need a new hot water heater or roof at some point. It is foolish and short sighted to not expect “unexpected” expenditures. Living in the moment and fulfilling your immediate desires may feel good today, but leaves you susceptible to disaster tomorrow. Gradually building a rainy day fund over time is what adults should do. Only immature children operate with no safety net. Everyone has an excuse for why they end up living on the edge, but the data exposes us to be an infantile nation of spendthrifts incapable of distinguishing between wants and needs. It might be understandable for young adults who are burdened by student loan debt and entry level jobs to have little or no savings, but the data for older Americans is most disturbing.

It seems 31% of all Generation X adults between the ages of 35 to 54, in the prime earning years of their lives, have ZERO savings, the highest among all age cohorts. Over 20% of them don’t even have a savings account. This is incomprehensible and reveals an almost juvenile approach to life. Approximately 70% of all 35 to 54 year old households have $1,000 or less in savings. These are people who should have been working for the last 10 to 30 years. To not have put aside more than $1,000 is beyond irresponsible, and the justification of earning no interest on savings is disingenuous as they could have earned 5% up until 2008. This shocking state of affairs can’t only be laid at the feet of the evil bankers and rich corporate titans.

Every person has to accept personal responsibility for their own life. There is one sure fire way to accumulate savings and that is to spend less than you earn. It sounds simple, but the vast majority of Americans have chosen to live beyond their means by allowing themselves to be lured into debt by the Wall Street debt peddlers and their Madison Avenue media maggots selling dreams to willfully ignorant delusional consumers. Consumer dependent corporations hawking autos, electronics, glittery baubles, fashionable attire, toxic processed sludge disguised as food, and other slave produced Chinese crap, require a vast unlimited supply of easy money debt to keep profits rolling in. And the Federal Reserve has been willing and able to accommodate them.

Those who control the levers of this perverted economic system utilize Fed easy money, propaganda advertising messages, and the susceptibility of an oblivious populace, suffering from delusions of grandeur, to create generations of debt enslaved hamsters running on the wheel of life. But, we were not forced into this enslavement. Millions have chosen to live lives of quiet desperation in order to keep up with the Joneses. They would rather portray themselves as successful and wealthy, rather than make the necessary sacrifices required to achieve success and wealth. Everyone has the ability to live beneath their means. Millions have made the choice to do so. The chart above shows 10% to 20% of people do have $10,000 or more in savings, including young people. Many are average middle class Americans, not the despised 1%.

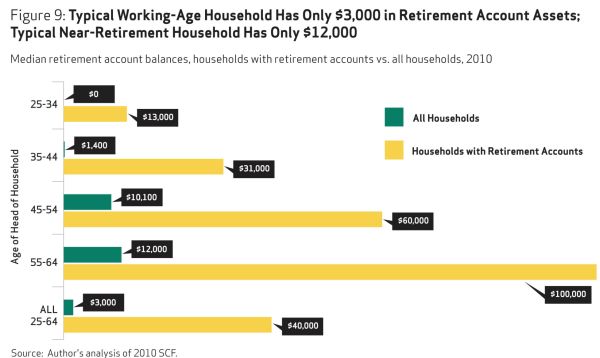

It is certainly not easy to accumulate savings in an economy stacked against the working middle class, but it is possible. It requires self-discipline, deferring gratification, patience, budgetary skills, staying employed, and not coveting your neighbors’ possessions. The lack of short-term savings is not an isolated data point. It is representative of a nation of narcissistic live for today ne’er-do-wells who rarely concern themselves with the future or the consequences of their actions. They haven’t been putting all their spare cash into their retirement plans either. When you realize the typical household between the ages of 35 to 54 has less than $10,000 saved for their retirement, the mass delusion becomes clear. How could Boomers, who have worked for 30 to 40 years, and experienced the greatest bull market in history (1981 – 2001) have only $12,000 of retirement savings as they approach retirement?

These are median figures, so half the households have even less retirement savings. It requires decades of living above your means to accumulate such little in savings. The apologists for the non-saving masses often argue Americans were utilizing their homes as a store of wealth to be used in retirement. This is just another false storyline, as the savings poor public used their homes like an ATM machine from 2001 through 2008, extracting hundreds of billions to spend on granite countertops, exotic Caribbean vacations, home theaters, BMWs, Olympic sized pools, bling, and new boobs for mommy. Equity in homes plunged from 60% to below 40% in the space of a few years and has only recovered to 55% after the Fed induced faux housing recovery. There are still millions of homeowners underwater, with the next leg down guaranteed to add millions more.